Medical device company Integra LifeSciences (NASDAQ: IART) missed Wall Street’s revenue expectations in Q3 CY2025, but sales rose 5.6% year on year to $402.1 million. Next quarter’s revenue guidance of $430 million underwhelmed, coming in 5.9% below analysts’ estimates. Its non-GAAP profit of $0.54 per share was 24.1% above analysts’ consensus estimates.

Is now the time to buy Integra LifeSciences? Find out by accessing our full research report, it’s free for active Edge members.

Integra LifeSciences (IART) Q3 CY2025 Highlights:

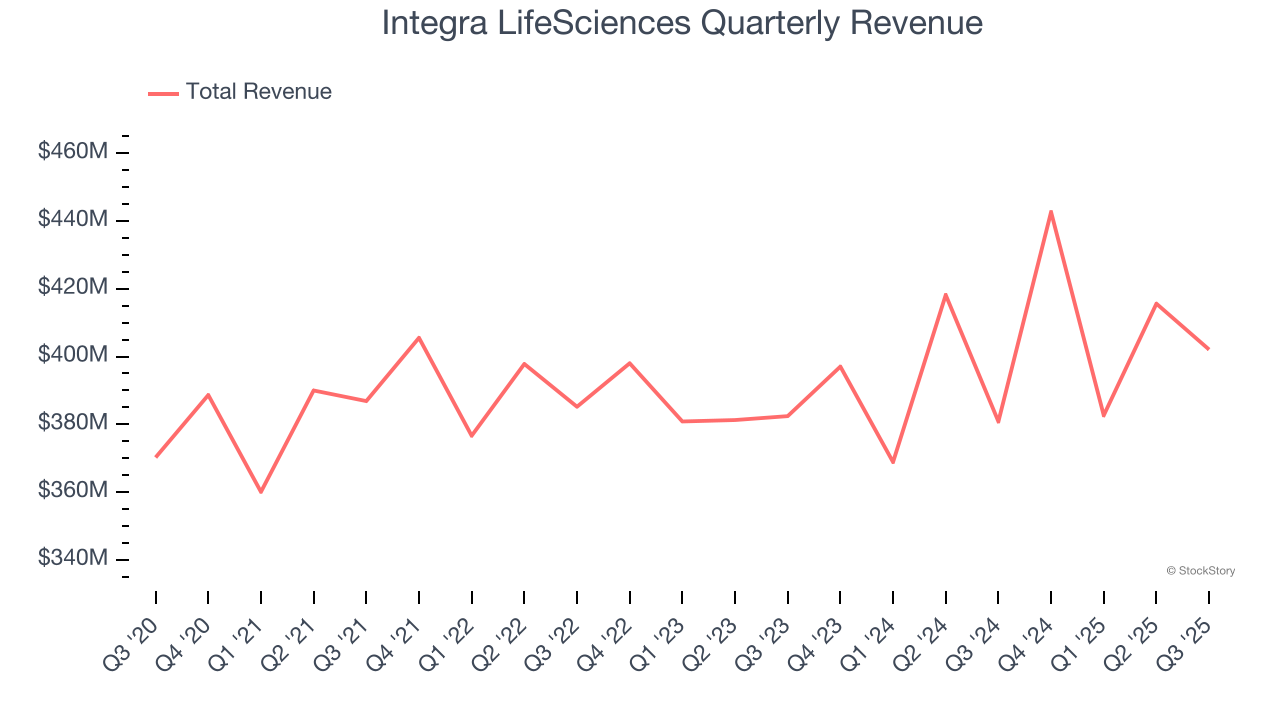

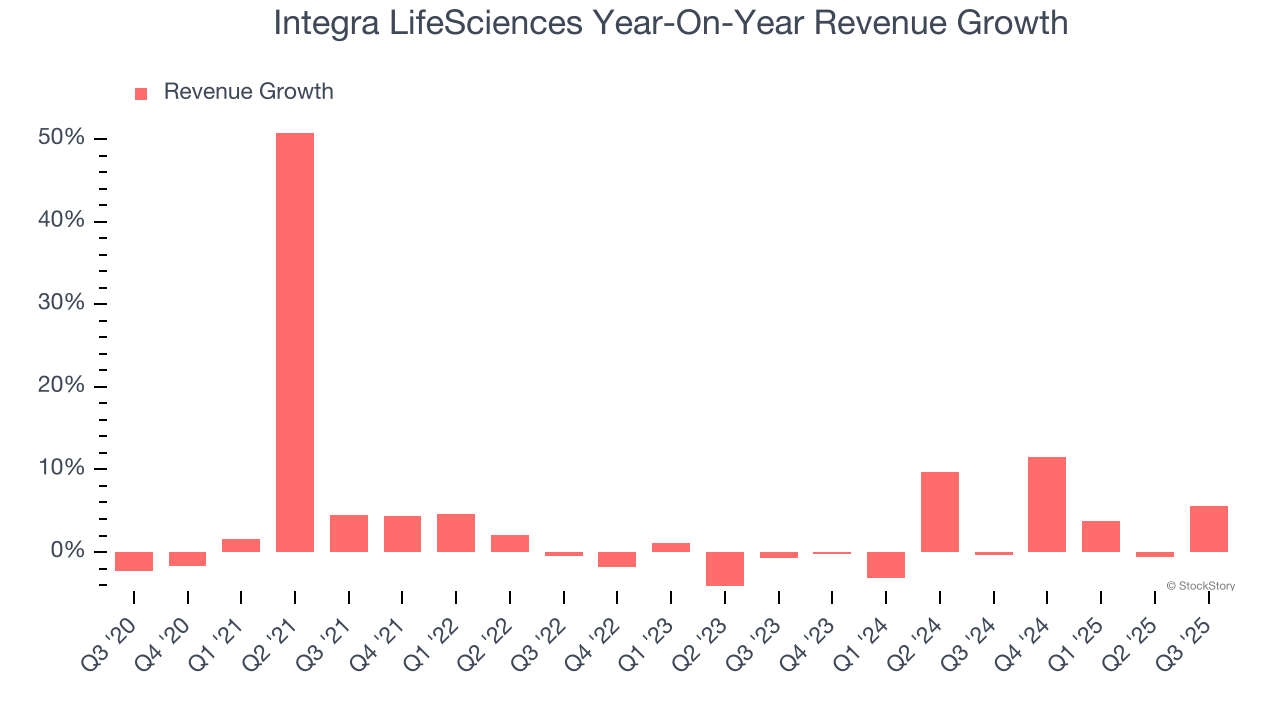

- Revenue: $402.1 million vs analyst estimates of $414.2 million (5.6% year-on-year growth, 2.9% miss)

- Adjusted EPS: $0.54 vs analyst estimates of $0.43 (24.1% beat)

- Adjusted EBITDA: $78.45 million vs analyst estimates of $68.79 million (19.5% margin, 14% beat)

- Revenue Guidance for Q4 CY2025 is $430 million at the midpoint, below analyst estimates of $457 million

- Management lowered its full-year Adjusted EPS guidance to $2.22 at the midpoint, a 1.1% decrease

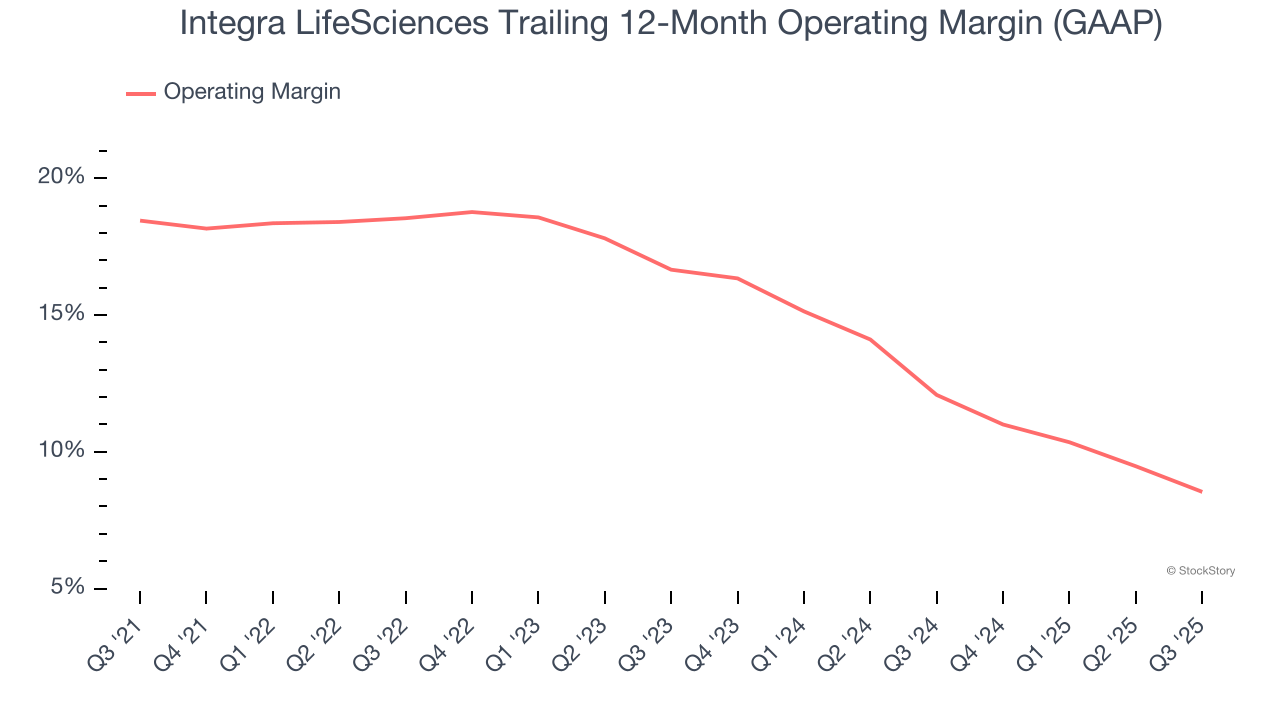

- Operating Margin: 2.9%, down from 6.6% in the same quarter last year

- Free Cash Flow was $25.75 million, up from -$7.16 million in the same quarter last year

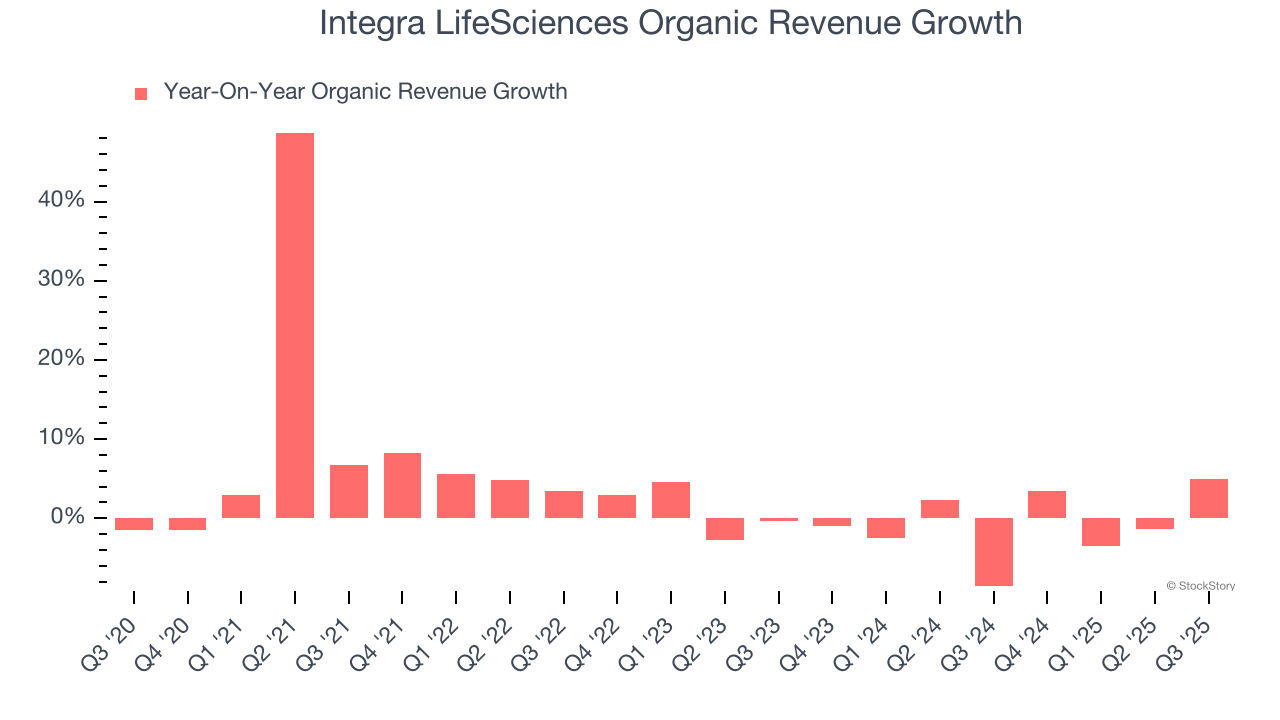

- Organic Revenue rose 5% year on year vs analyst estimates of 8.4% growth (339.7 basis point miss)

- Market Capitalization: $1.20 billion

“In the third quarter, we continued to see healthy demand across our portfolio. While revenue was impacted by two supply interruptions, we delivered strong profitability and cash flow through disciplined cost management and operational efficiencies.” said Mojdeh Poul, president and chief executive officer.

Company Overview

Founded in 1989 as a pioneer in regenerative medicine technology, Integra LifeSciences (NASDAQ: IART) develops and manufactures medical technologies for neurosurgery, wound care, and surgical reconstruction, including regenerative tissue products and surgical instruments.

Revenue Growth

A company’s long-term sales performance can indicate its overall quality. Any business can have short-term success, but a top-tier one grows for years. Regrettably, Integra LifeSciences’s sales grew at a tepid 3.6% compounded annual growth rate over the last five years. This was below our standard for the healthcare sector and is a rough starting point for our analysis.

Long-term growth is the most important, but within healthcare, a half-decade historical view may miss new innovations or demand cycles. Integra LifeSciences’s annualized revenue growth of 3.2% over the last two years aligns with its five-year trend, suggesting its demand was consistently weak.

Integra LifeSciences also reports organic revenue, which strips out one-time events like acquisitions and currency fluctuations that don’t accurately reflect its fundamentals. Over the last two years, Integra LifeSciences’s organic revenue was flat. Because this number is lower than its two-year revenue growth, we can see that some mixture of acquisitions and foreign exchange rates boosted its headline results.

This quarter, Integra LifeSciences’s revenue grew by 5.6% year on year to $402.1 million, missing Wall Street’s estimates. Company management is currently guiding for a 2.9% year-on-year decline in sales next quarter.

Looking further ahead, sell-side analysts expect revenue to grow 4.8% over the next 12 months. While this projection indicates its newer products and services will catalyze better top-line performance, it is still below the sector average.

Here at StockStory, we certainly understand the potential of thematic investing. Diverse winners from Microsoft (MSFT) to Alphabet (GOOG), Coca-Cola (KO) to Monster Beverage (MNST) could all have been identified as promising growth stories with a megatrend driving the growth. So, in that spirit, we’ve identified a relatively under-the-radar profitable growth stock benefiting from the rise of AI, available to you FREE via this link.

Operating Margin

Operating margin is an important measure of profitability as it shows the portion of revenue left after accounting for all core expenses – everything from the cost of goods sold to advertising and wages. It’s also useful for comparing profitability across companies with different levels of debt and tax rates because it excludes interest and taxes.

Integra LifeSciences has done a decent job managing its cost base over the last five years. The company has produced an average operating margin of 14.8%, higher than the broader healthcare sector.

Looking at the trend in its profitability, Integra LifeSciences’s operating margin decreased by 9.9 percentage points over the last five years. The company’s two-year trajectory also shows it failed to get its profitability back to the peak as its margin fell by 8.1 percentage points. This performance was poor no matter how you look at it - it shows its expenses were rising and it couldn’t pass those costs onto its customers.

This quarter, Integra LifeSciences generated an operating margin profit margin of 2.9%, down 3.7 percentage points year on year. This contraction shows it was less efficient because its expenses grew faster than its revenue.

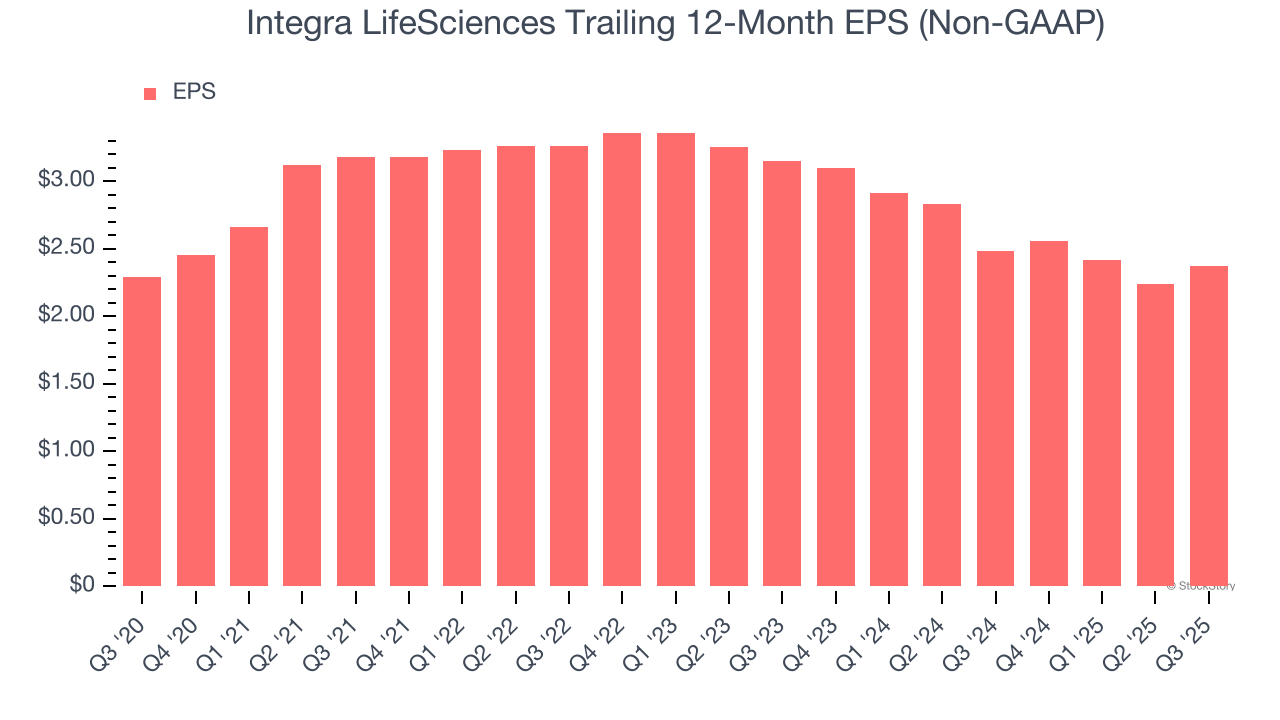

Earnings Per Share

Revenue trends explain a company’s historical growth, but the long-term change in earnings per share (EPS) points to the profitability of that growth – for example, a company could inflate its sales through excessive spending on advertising and promotions.

Integra LifeSciences’s flat EPS over the last five years was below its 3.6% annualized revenue growth. This tells us the company became less profitable on a per-share basis as it expanded due to non-fundamental factors such as interest expenses and taxes.

We can take a deeper look into Integra LifeSciences’s earnings to better understand the drivers of its performance. As we mentioned earlier, Integra LifeSciences’s operating margin declined by 9.9 percentage points over the last five years. This was the most relevant factor (aside from the revenue impact) behind its lower earnings; interest expenses and taxes can also affect EPS but don’t tell us as much about a company’s fundamentals.

In Q3, Integra LifeSciences reported adjusted EPS of $0.54, up from $0.41 in the same quarter last year. This print easily cleared analysts’ estimates, and shareholders should be content with the results. Over the next 12 months, Wall Street expects Integra LifeSciences’s full-year EPS of $2.37 to grow 8.5%.

Key Takeaways from Integra LifeSciences’s Q3 Results

It was good to see Integra LifeSciences beat analysts’ EPS expectations this quarter. On the other hand, its revenue guidance for next quarter missed and its revenue fell short of Wall Street’s estimates. Overall, this quarter could have been better. The stock traded down 4.4% to $14.75 immediately after reporting.

Integra LifeSciences underperformed this quarter, but does that create an opportunity to invest right now? If you’re making that decision, you should consider the bigger picture of valuation, business qualities, as well as the latest earnings. We cover that in our actionable full research report which you can read here, it’s free for active Edge members.